Skip to content

Who We Are

About BOI

Our People

Management Team

Our Organogram

Our Locations

Sustainability

Corporate Social Responsibility

Corporate Strategy

Thematic Areas

Our Subsidiaries

Partners

What We Offer

Short, Medium and Long Term Financing

Business Advisory

Project Support

FGN MSME Intervention Program

iDICE

NLNG-BOI Matching Fund

RAPID

Impact

Media

Investor Relations

times

Who We Are

About BOI

Our People

Management Team

Our Organogram

Our Locations

Sustainability

Corporate Social Responsibility

Corporate Strategy

Thematic Areas

Our Subsidiaries

Partners

What We Offer

Short, Medium and Long Term Financing

Business Advisory

Project Support

FGN MSME Intervention Program

iDICE

NLNG-BOI Matching Fund

RAPID

Impact

Media

Investor Relations

reportgov

.ng

BLOG

Opinions & Insights shared by our Expert Team Members

Categories

2018

2018

2019

2019

2020

2021

2021

2021

2022

2022

2023

2024

2025

2026

Annual Reports

Audits

Blog Posts

BOI Impact Stories

BOI in the Press

Business

Business

Entertainment

Industry Reports

Industry Reports

Investor Relations

journals

Media & News

New Videos

News

News & Events

Old Videos

Past Events

Press Releases

Publications

Resources

Technology

Technology

UnAssigned

Uncategorized

Search

15 May

Bank of Industry Limited and IFC Sign Agreement to Assess Development of Major Conference and Exhibition Hub in Abuja

Read more

15 May

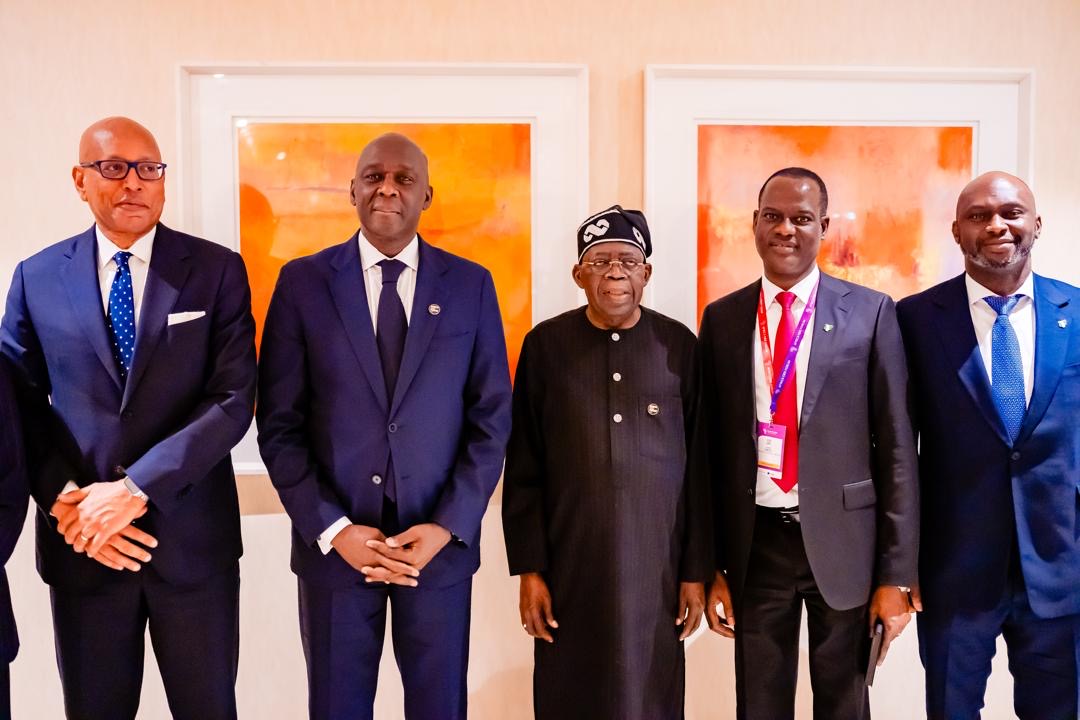

BOI MD/CEO Dr. Olasupo Olusi Joins President Bola Ahmed Tinubu and Global Development Leaders at Africa CEO Forum 2026

Read more

13 May

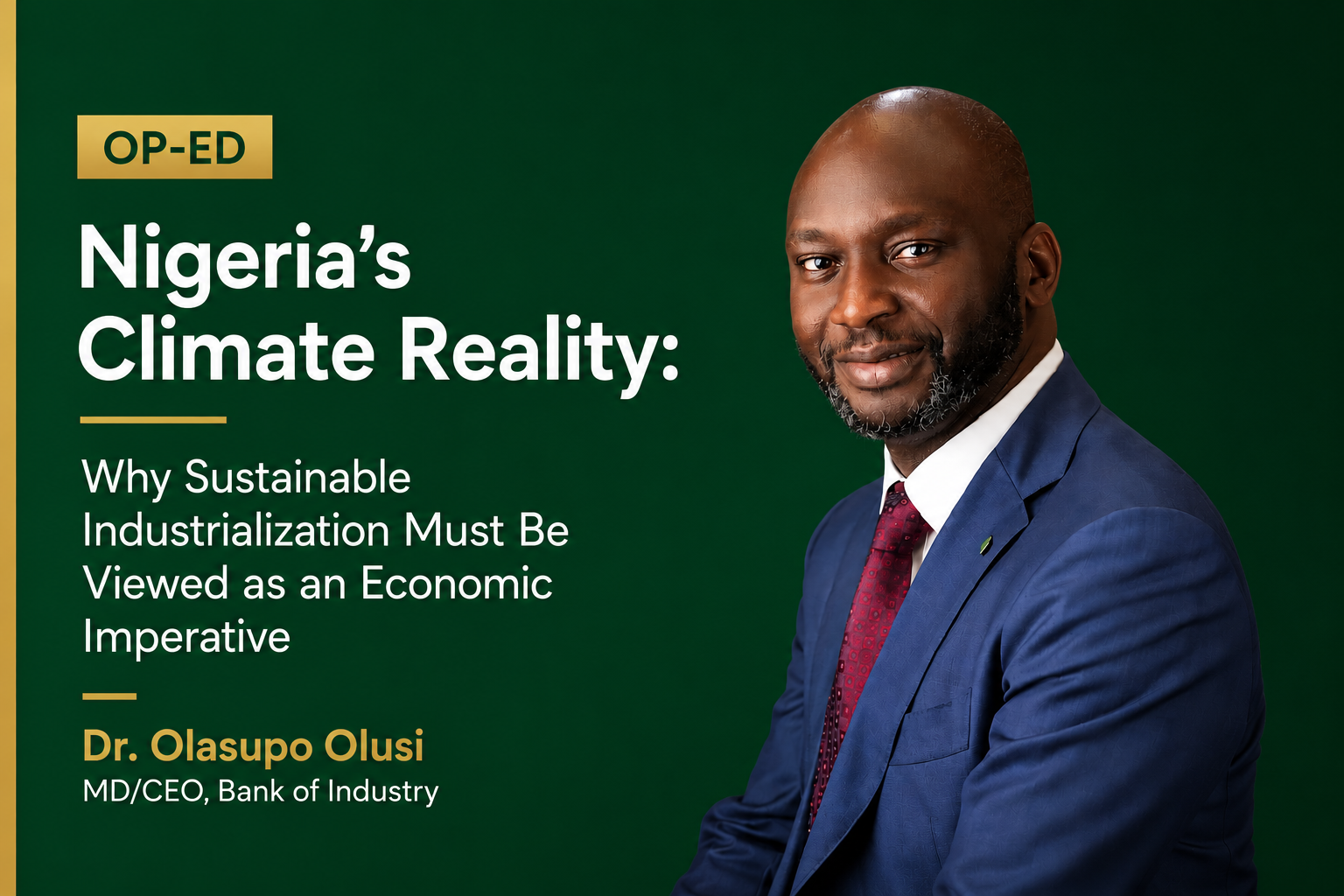

Op-Ed: Nigeria’s Climate Reality: Why Sustainable dustrialization Must Be Viewed as an Economic Imperative

Read more

11 May

Olasupo Olusi: Repositioning BOI as Engine of Industrial Growth

Read more

22 Apr

Bank of Industry Wins 2026 Sustainable Finance Award by Global Finance Magazine for Circular Economy Leadership

Read more

22 Apr

From Raw Materials to Finished Products: BOI and RMRDC Sign Strategic Partnership

Read more

22 Apr

BOI Partners with GIZ to Expand Access to Finance for Nigerian MSMEs

Read more

22 Apr

Empowering Growth: BOI Hosts Micro Lending Customer Forum in Kano

Read more

22 Apr

Celebrating Excellence: BOI Hall of Fame & BDSP Awards 2026

Read more

Load More

Language »

Search

About BOI

Our People

Executive Management

Our Organogram

Our Locations

Sustainability

Corporate Social Responsibility

Corporate Strategy

Thematic Areas

BOI Partners

Short, Medium and Long Term Financing

MSMEs

Large Enterprises

Public Sector & Interventions Program

FGN MSME Intervention Program

Investor Relations

Business Advisory [BDSPs]

Projects

FGN MSME Intervention Program

iDICE

BRAVE

NLNG-BOI Matching Fund

RAPID

Customer Support

Customer Support

Whistleblowing Portal

Careers

Products

SMEs

Public Sector & Intervention Programmes

Large Enterprises

Impact

Media

Blog Posts

Policies

Anti Bribery & Corruption Policy

BCMS Policy Statement

BOI Anti-Fraud, Anti-Bribery & Anti-Corruption Policy Statement

ISMS – PIMS External Policy

Quality Policy Statement

Whistleblowing Policy

Subsidiaries

BOI Insurance Brokers

BOI LECON

BOI Microfinance Bank

BOI Investment & Trust Company

Close

WHO ARE WE

About BOI

Our People

Executive Management

Our Locations

Sustainability

Corporate Social Responsibility

Corporate Strategy

Our Thematic Areas

BOI Partners

WHAT WE OFFER

Short, Medium and Long Term Financing

Large Enterprises

MSMEs

Public Sector & Interventions Program

Business Advisory [BDSP]

Projects

FGN MSME Intervention Program

IDICE

RAPID

NGNG-BOI Matching Fund

BRAVE

Customer Support

Careers

PRODUCTS

BOI Products/Funds

IMPACT

INVESTOR RELATIONS

MEDIA

Photos & Videos

Blog Posts

POLICIES

Policies

Anti bribery & Corruption

Anti-Fraud, Anti-Bribery & Anti-Corruption Policy Statement

ISMS-PIMS External Policy

Quality Policy Statement

Whistleblowing Policy

BCMS Policy Statement

ANNUAL REPORTS & JOURNALS

Annual Reports

Journal of Development Review

Journal of Development Finance

SUBSIDIARIES

BOI ITC

BOI Microfinance

BOI Insurance Brokers

BOI LECON

BOI PRICE SENSE

REPORT GOV

WHO ARE WE

About BOI

Our People

Executive Management

Our Locations

Sustainability

Corporate Social Responsibility

Corporate Strategy

Our Thematic Areas

BOI Partners

WHAT WE OFFER

Short, Medium and Long Term Financing

Large Enterprises

MSMEs

Public Sector & Interventions Program

Business Advisory [BDSP]

Projects

FGN MSME Intervention Program

IDICE

RAPID

NGNG-BOI Matching Fund

BRAVE

Customer Support

Careers

PRODUCTS

BOI Products/Funds

IMPACT

INVESTOR RELATIONS

MEDIA

Photos & Videos

Blog Posts

POLICIES

Policies

Anti bribery & Corruption

Anti-Fraud, Anti-Bribery & Anti-Corruption Policy Statement

ISMS-PIMS External Policy

Quality Policy Statement

Whistleblowing Policy

BCMS Policy Statement

ANNUAL REPORTS & JOURNALS

Annual Reports

Journal of Development Review

Journal of Development Finance

SUBSIDIARIES

BOI ITC

BOI Microfinance

BOI Insurance Brokers

BOI LECON

BOI PRICE SENSE

REPORT GOV

SMEs

Youth & Skills

Digital Economy

Climate

Infrastructure

Gender

Operationalizing Them

Environmental & Risk Management

Climate

Partnerships for Change

Environmental & Risk Management

Climate

Partnerships for Change

Our Locations

Board of Directors

Executive Management Team

BOI History

Our Story

Our Values

Why Choose BOI

Market Focus

Impact

Our Partners

BOI ITIC

BOI Microfinance

BOI Insurance Brokers

LECON

BCMS Policy Statement

Whistleblowing Policy

Anti bribery & Corruption

Anti fraud, bribery & corruption policy statement

Quality Policy Statement

ISMS Statment

Photos

Videos

News & Events

Blog Posta

Success Stories

Testimonials

Awards and Recognition

BOI Products/Funds

Matching Funds

Managed/Intervention Funds

Short, Medium and

Long Term Financing

Investor Relations

Business Advisory [BDSP]

Projects

Customer Support

Careers

Close

WHO WE ARE

WHAT WE OFFER

PRODUCTS

IMPACT

MEDIA

Policies

Subsidiaries

Investor Relations