Skip to content

Menu

Report Gov

Apply for a loan

BLOG

Opinions & Insights shared by our Expert Team Members

Categories

2018

2018

2019

2019

2020

2021

2021

2021

2022

2022

2023

2024

2025

Annual Reports

Audits

Blog Posts

BOI in the Press

Business

Business

Entertainment

Industry Reports

Industry Reports

Investor Relations

journals

Media & News

New Videos

News

News & Events

Old Videos

Past Events

Press Releases

Publications

Resources

Technology

Technology

UnAssigned

Search

02 Apr

Bank of Industry Wins ‘Syndicated Loan Deal of the Year’ at the Global Banking & Markets Africa Awards

Read more

04 Mar

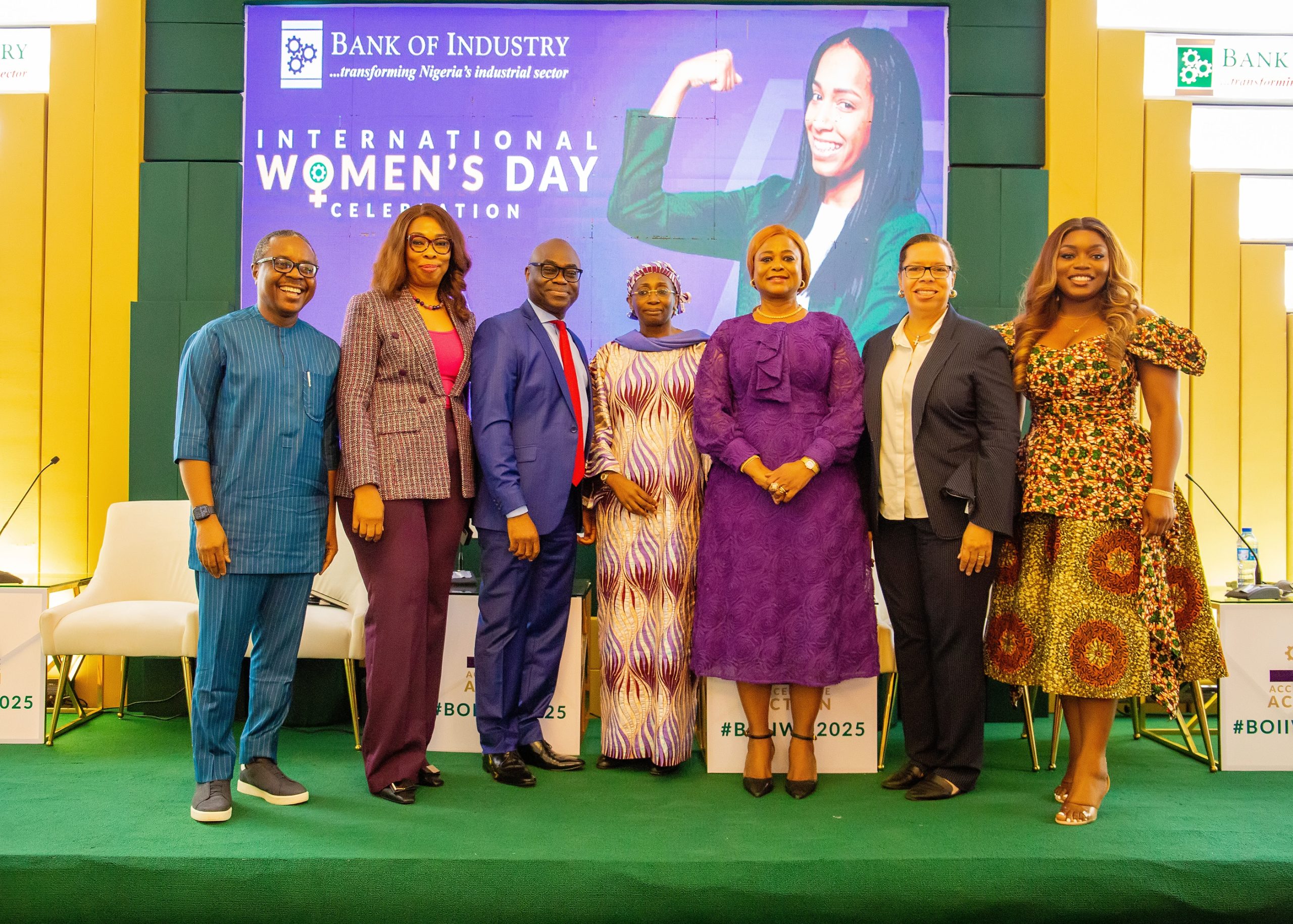

BOI Celebrates International Women’s Day

Read more

28 Feb

BOI Strengthens Partnership with UN Global Compact to Drive Sustainable Development

Read more

29 Jan

BOI wins ‘Transaction of the Year’ award at the 2025 ThisDay Awards

Read more

17 Dec

BOI is honoured Best Company in Financial Inclusion award at the SERAS CSR Awards

Read more

12 Dec

BOI Loan Portfolio Guarantee Agreement with AGF

Read more

20 Nov

BOI Celebrates International Men’s Day

Read more

15 Oct

BOI Journal of Development Finance Vol 1 No. 1

Read more

15 Oct

BOI Journal of Development Review Vol 1

Read more

Load More

Close

WHO WE ARE

WHAT WE OFFER

PRODUCTS

IMPACT

MEDIA

Policies

Subsidiaries

Annual reports

Search

Close

WHO ARE WE

About BOI

Our People

Executive Management

Our Locations

Sustainability

Corporate Social Responsibility

Corporate Strategy

Our Thematic Areas

BOI Partners

WHAT WE OFFER

Short, Medium and Long Term Financing

Large Enterprises

MSMEs

Public Sector & Interventions Program

Investor Relations

Business Advisory [BDSP]

Projects

FGN MSME Intervention Program

IDICE

RAPID

NGNG-BOI Matching Fund

BRAVE

Customer Support

Careers

PRODUCTS

BOI Products/Funds

IMPACT

MEDIA

Photos & Videos

Blog Posts

POLICIES

Policies

Anti bribery & Corruption

Anti-Fraud, Anti-Bribery & Anti-Corruption Policy Statement

BCMS Policy Statement

ISMS-PIMS Executive Support Statement

Quality Policy Statement

Whistleblowing Policy

ANNUAL REPORTS & JOURNALS

Annual Reports

Journal of Development Review

Journal of Development Finance

SUBSIDIARIES

BOI ITC

BOI Microfinance

BOI Insurance Brokers

BOI LECON

BOI PRICE SENSE

REPORT GOV

WHO ARE WE

About BOI

Our People

Executive Management

Our Locations

Sustainability

Corporate Social Responsibility

Corporate Strategy

Our Thematic Areas

BOI Partners

WHAT WE OFFER

Short, Medium and Long Term Financing

Large Enterprises

MSMEs

Public Sector & Interventions Program

Investor Relations

Business Advisory [BDSP]

Projects

FGN MSME Intervention Program

IDICE

RAPID

NGNG-BOI Matching Fund

BRAVE

Customer Support

Careers

PRODUCTS

BOI Products/Funds

IMPACT

MEDIA

Photos & Videos

Blog Posts

POLICIES

Policies

Anti bribery & Corruption

Anti-Fraud, Anti-Bribery & Anti-Corruption Policy Statement

BCMS Policy Statement

ISMS-PIMS Executive Support Statement

Quality Policy Statement

Whistleblowing Policy

ANNUAL REPORTS & JOURNALS

Annual Reports

Journal of Development Review

Journal of Development Finance

SUBSIDIARIES

BOI ITC

BOI Microfinance

BOI Insurance Brokers

BOI LECON

BOI PRICE SENSE

REPORT GOV

About BOI

Our People

Executive Management

Our Locations

Sustainability

Corporate Social Responsibility

Corporate Strategy

Thematic Areas

BOI Partners

Short, Medium and Long Term Financing

MSMEs

Large Enterprises

Public Sector & Interventions Program

FGN MSME Intervention Program

Investor Relations

Business Advisory [BDSPs]

Projects

FGN MSME Intervention Program

iDICE

BRAVE

NLNG-BOI Matching Fund

RAPID

Customer Support

Customer Support

Whistleblowing Portal

Careers

Products

SMEs

PSIP

Large Enterprises

Impact

Media

Blog Posts

Policies

Anti Bribery & Corruption Policy

BOI Anti-Fraud, Anti-Bribery & Anti-Corruption Policy Statement

BCMS Policy Statement

ISMS – PIMS Executive Support Statement

Quality Policy Statement

Whistleblowing Policy

Subsidiaries

BOI Insurance Brokers

BOI LECON

BOI Microfinance Bank

BOI Investment & Trust Company

Board of Directors

Executive Management Team

Short, Medium and

Long Term Financing

Investor Relations

Business Advisory [BDSP]

Projects

Customer Support

Careers

BOI Products/Funds

Matching Funds

Managed/Intervention Funds

Success Stories

Testimonials

Awards and Recognition

Photos

Videos

News & Events

Blog Posta

BCMS Policy Statement

Whistleblowing Policy

Anti bribery & Corruption

Anti fraud, bribery & corruption policy statement

Quality Policy Statement

ISMS Statment

BOI ITIC

BOI Microfinance

BOI Insurance Brokers

LECON

Our Story

Our Values

Why Choose BOI

Market Focus

Impact

Our Partners

BOI History

Our Locations

Environmental & Risk Management

Climate

Partnerships for Change

Environmental & Risk Management

Climate

Partnerships for Change

SMEs

Youth & Skills

Digital Economy

Climate

Infrastructure

Gender

Operationalizing Them